Private Credit

Private Credit

The banking loan alternative at $1.5T and growing,

Like many growing their business, I encountered a troublesome traditional banker who presented hurdles in securing a loan for my financial investment platform due to banking restrictions on software-based businesses. The slow process delayed my growth plans by six months. While private credit, as I now know it, did not exist, I was able to secure a suitable custom arrangement, which the credit investor ended up with incredible returns.

The previous traditional banking lender, learning of my success, was suddenly open and ready to work out a deal that would have been far less ideal. Of course, I declined the lender's interest, and that bank lost an incredible amount of future business.

Let’s learn about Private credit and the opportunities and risks for companies and credit investors.

Introduction

Private credit (PC) is another alternative investment that involves lending money to private borrowers, including companies, individuals, or funds not listed on public markets.

Private credit investors receive interest payments and principal repayments from the borrowers, as well as collateral or other forms of security in case of default. PC can offer higher interest rates, lower volatility, and diversification benefits compared to traditional fixed-income investments2.

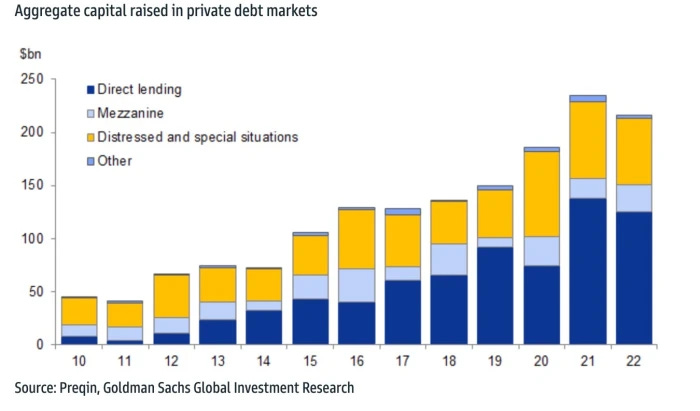

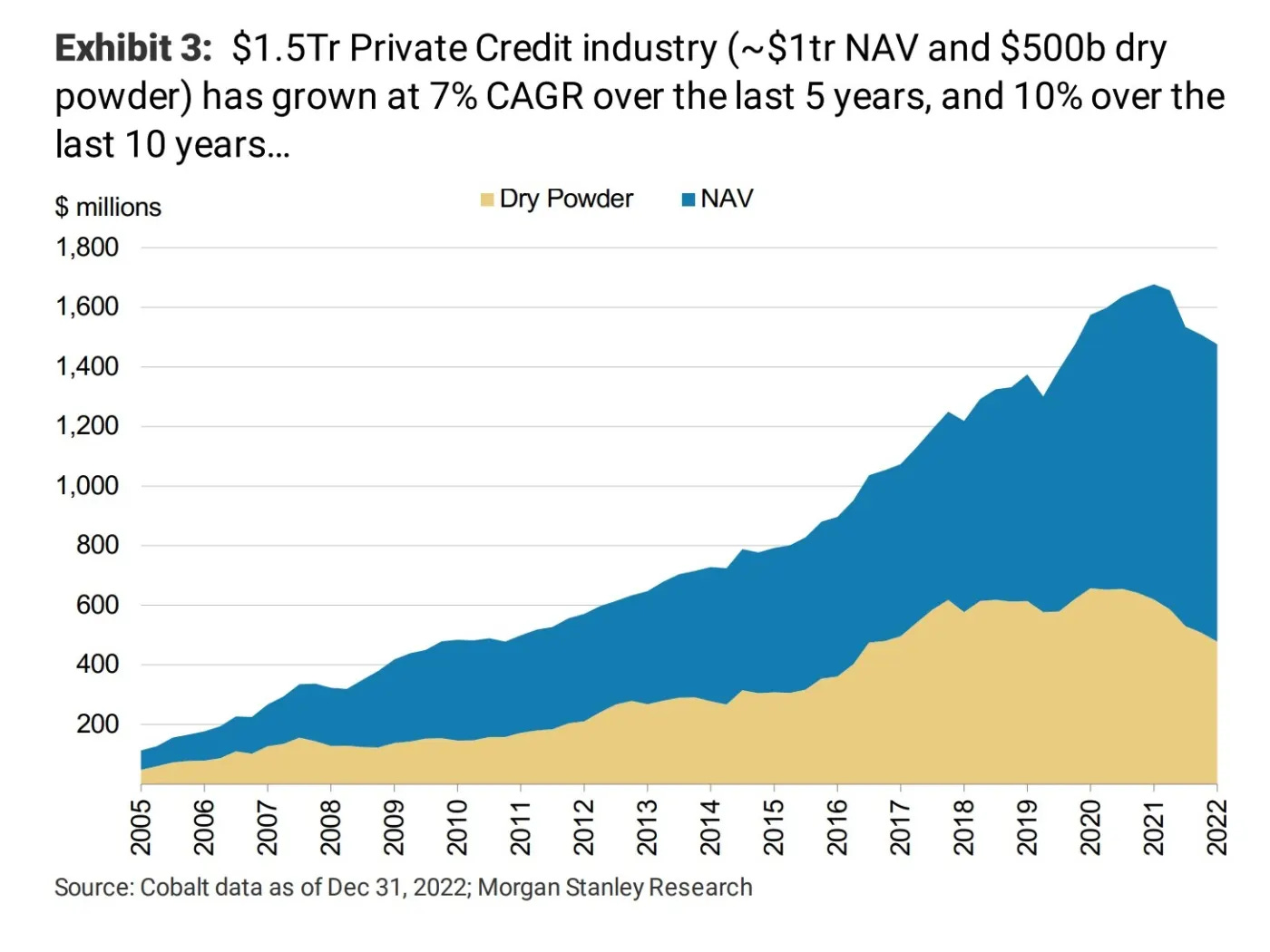

According to Morgan Stanley, the size of the private credit market at the start of 2023 was approximately $1.4 trillion, compared to $875 billion in 2020, and is estimated to grow to $2.3 trillion by 20271.

A study by UNC Kenan-Flagler Business School and Emory University analyzed the performance of 476 private credit funds, including a subset of 155 direct lending funds, from 2004 to 2018. They found that the average net internal rate of return (IRR) for private credit funds was 11.4%, while the average net IRR for direct lending funds was 9.5%23.

A report by Cambridge Associates described the different types of private credit strategies and their risk/return profiles. They showed that private credit strategies such as direct lending, mezzanine, and distressed debt had higher returns and lower volatility than public high-yield bonds and leveraged loans from 2005 to 20194.

Similarities Between PC and PE

Both private credit and private equity are alternative investments that also have similarities in terms of risk, return, liquidity, and duration, such as:

Offer higher returns than traditional investments but involve higher risks and require higher minimum investments.

Have lower liquidity, meaning they cannot be quickly sold or converted into cash, and require investors to lock in their capital for a long time.

Have longer investment horizons and depend on the performance and exit of the underlying assets.

Subject to various regulations and legal frameworks, depending on the jurisdiction, the type of borrower, and the type of instrument.

Difference between PC and PE

The primary difference is that private credit investors lend money to borrowers and receive interest payments. Private equity investors buy ownership stakes in companies and aim to sell them for a profit. Private credit is a type of debt financing, while private equity is a type of equity financing123.

Private credit and private equity are both types of alternative investments that are not traded on public markets. They are both private investments, which means they are similar in some respects, but they are also different in critical ways4.

Some of the other differences between private credit and private equity are:

Risk and return: Private credit offers more predictable and stable returns, as the interest payments are fixed and contractual. Private equity has higher upside potential, as the value of the companies can increase significantly over time. Remember that private equity also has higher risk, as the companies may perform poorly or fail to exit successfully.

Liquidity and duration: Private credit is less liquid than private equity, as the loans are usually locked in for a certain period and have limited secondary markets. Private equity can be more liquid than private credit, as the investors can sell their shares or take the companies public when the opportunity arises. However, private equity also has a longer duration than private credit, as the investors have to wait for the companies to mature and exit.

Involvement and influence: Private credit investors have limited involvement and influence in the management of the borrowers, as they mainly focus on credit quality and repayment ability. Private equity investors have more involvement and influence in the management of the companies, as they often provide strategic guidance, operational improvement, and governance oversight.

Popularization

With financial and policy changes, Private equity and private credit have become popular.

These do happen in cycles. Here are some of the reasons for the growth of these asset classes:

Low-interest rates: Since the global financial crisis of 2008, central banks have kept interest rates low to stimulate the economy. This has reduced the returns of traditional fixed-income investments, such as bonds, and increased the demand for alternative sources of income, such as private credit. Private credit can offer higher yields and floating rates that adjust to market conditions12

Regulatory changes: After the financial crisis, banks faced stricter regulations and capital requirements that limited their ability to lend to certain sectors and borrowers. This created a gap in the credit market filled by non-bank lenders, such as private credit funds. Private credit funds can offer more customized and flexible solutions to borrowers who may have difficulty accessing credit from banks or the public market12

Private equity expansion: Private equity has been one of the best-performing asset classes in the past two decades, delivering higher returns than public equity markets. This has attracted more capital and investors to the private equity industry, which in turn has increased the demand for private credit to finance buyouts, acquisitions, and growth strategies. Private credit funds can partner with private equity sponsors to provide debt financing for their portfolio companies13.

As a note VC has outperformed over the golden decade after the financial crisis, however much of that performance has been limited to a small percentage of funds. According to Cambridge Associates, private equity (PE) had an average annual return of 14.65% from 2001 to 2021, while venture capital (VC) had an average annual return of 11.53% over the same period. However, venture capital was the top performer from 2010 to 2020, with an average annual return of 15.15%.Diversification benefits: Both private equity and private credit can offer diversification benefits to investors, as they have a low correlation with public markets and can generate returns across different economic cycles. Private equity can capture the value creation and operational improvement of private companies, while private credit can provide stable income and downside protection14

Don’t forget that these asset classes also involve higher risks, fees, and illiquidity than traditional investments and require careful due diligence and selection. Investors should be aware of the potential benefits and challenges of investing in private equity and private credit12

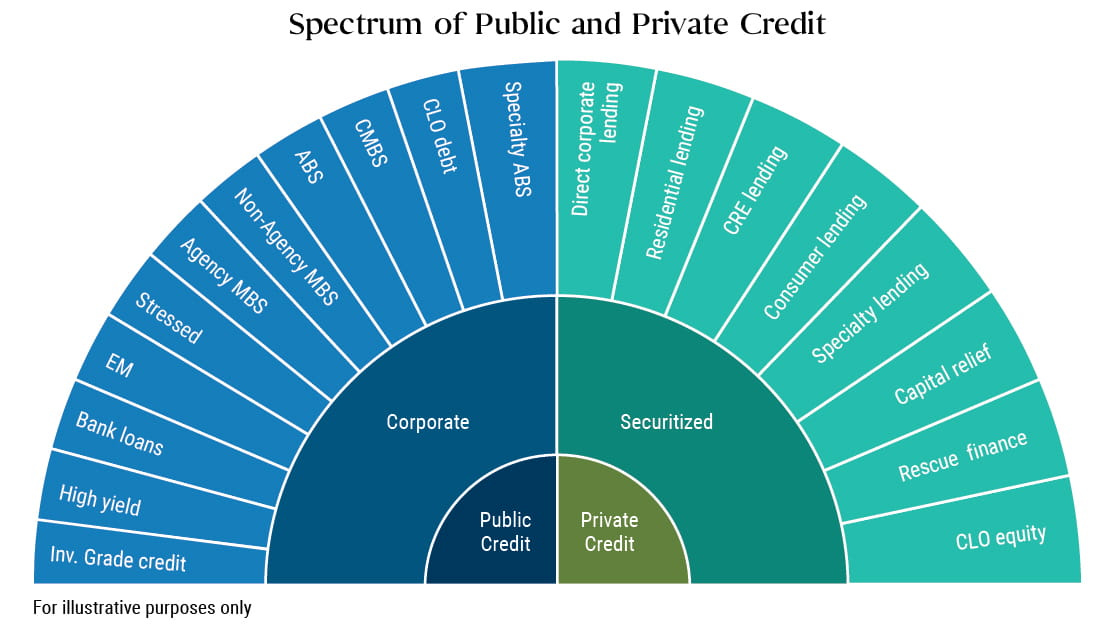

Types of Private Credit

There are generally four common types of private credit1:

Direct lending: Direct lending strategies provide credit primarily to private, non-investment-grade companies. Direct lending strategies may be appealing as they invest in the senior-most part of a company’s capital structure, which may provide steady current income with relatively lower risk.

Mezzanine financing: Mezzanine financing is a form of subordinated debt that provides borrowers with additional capital beyond what senior lenders are willing to provide. Mezzanine financing often comes with equity “kickers”, which are incentives that can support attractive total returns, while still being a debt claim in the payment waterfall.

Distressed debt: Distressed debt is a type of debt that trades at a significant discount to its face value due to the financial distress or bankruptcy of the issuer. Distressed debt investors seek to profit from the recovery or restructuring of the issuer or from the liquidation of its assets.

Specialty finance: Specialty finance is a broad term that covers various types of niche lending that traditional banks do not typically offer. Specialty finance can include lending against specialized assets such as railcars and airplanes or contractual revenue streams like royalties and subscription services.

The sources of private credit can vary depending on the type and size of the borrower, the availability and cost of capital, and the regulatory environment. Some of the sources of private credit are:

Private credit and debt funds: These are funds that raise capital from institutional and individual investors and deploy it in various private credit strategies. They can offer access to a diversified portfolio of private credit investments, professional management, and expertise.

Nonbank lenders: These are entities that provide credit to borrowers without being regulated as banks. They can include insurance companies, pension funds, hedge funds, business development companies, and online platforms. They can offer more flexibility, speed, and customization than banks, as well as lower fees and higher returns.

Banks: Banks are still involved in the private credit market, although to a lesser extent than before the Global Financial Crisis. Banks can provide credit to borrowers directly or through intermediaries such as private credit funds or nonbank lenders. Banks can also act as arrangers, underwriters, or agents for private credit transactions.

Private Credit Risks

Some risks and challenges related to private credit are very similar to other private market investing, such as12345:

Credit quality: PC investors have to assess the creditworthiness and repayment ability of the borrowers, which can be difficult due to the lack of publicly available information, the complexity of the transactions, and the potential for fraud or misrepresentation. Private credit investors also have to monitor the performance and financial health of the borrowers and deal with any defaults or restructurings that may occur.

Liquidity: As mentioned before, PC investments are usually illiquid, meaning they cannot be quickly sold or converted into cash. Private credit investors have to lock in their capital for a certain period, typically ranging from a few years to a decade or more and have limited options to exit or redeem their investments. Private credit investments also have limited secondary markets, meaning they may trade at a significant discount to their fair value if sold before maturity.

Regulation: Private credit investments are subject to various regulations and legal frameworks, depending on the jurisdiction, the type of borrower, and the type of instrument. Investors have to comply with the rules and requirements of the regulators, such as reporting, disclosure, taxation, and licensing. Also, PC investors have to deal with the risks and uncertainties of changing regulations, which may affect the availability, cost, and terms of private credit.

As a note, as Private Credit has developed critical mass, it’s beginning to compete with banks and the federal regulations set for them. Watch carefully how federal and international regulators navigate the competition to balance special interests, policies, and consumer & SMB advocacy.

Future

Private equity will benefit from attractive investment opportunities as many companies seek to recover, restructure, or transform their businesses in the post-pandemic era. Also, they will undoubtedly begin to see greater deal flow as many VC firms begin shedding their portfolio companies either to streamline or navigate their fund performance. Where they are struggling is that as of the beginning of 2024, there has been a hangover from the overvaluation period with significant cash investments from 2021/22, which flowed into many companies.

This, however, could be compounded by the opportunity with Private Credit.

Companies accustomed to the ZIRP era will seek out alternative sources of financing to continue operations without diluting or conducting an LBO or IPO. Also, traditional lenders have become more cautious and selective in the aftermath of the COVID-19 pandemic.

On the flip side, for investors holding on to unprecedented amounts of cash, private credit can offer attractive returns, diversification, and protection from inflation and market volatility.

Technology, healthcare, and finance have been the three areas most ripe for both private equity and private credit, but PC is taking a greater attraction for its structured, moderate-risk, short-term with relatively predictable returns.

The biggest risk remains to be defaults. So it’s crucial to evaluate quality companies and ensure lending firms/investors of private credit have the right team, tools and thesis to minimize those risks. While much of the PC is senior debt, that debt is still at considerable risk with the other lenders and investors. As private credit becomes more popular, a rising tide effect may occur for increased competition at lower margins.

And now…

I’ve invested in one firm and navigated investments to another firm delivering private credit. So far, the interest returns have been a nice inflow. My only concerns have been the opportunity cost of those investment dollars. It’s probably the high from the recent increases in the markets and VC returns, but diversification in PE and PC are sound strategies. Also, I have set up an arrangement to offer private credit to a mid-size healthcare company in lieu of a six-figure equity and advisory/consultative compensation. I will keep you posted on how these go.

How do you see the dynamics of company sources of funding shifting with Private Credit?